Emma Taylor- I am a passionate personal finance blogger dedicated to helping individuals take control of their financial well-being.

Emma Taylor- I am a passionate personal finance blogger dedicated to helping individuals take control of their financial well-being.Not long ago, a residence in the picturesque Forest Hill area of San Francisco hit the market with a $2.4 million asking price. This four-bedroom, three-bathroom property spanned a humble 2,250 square feet and had undergone renovations roughly 15 years prior. As is our custom at every open house, my

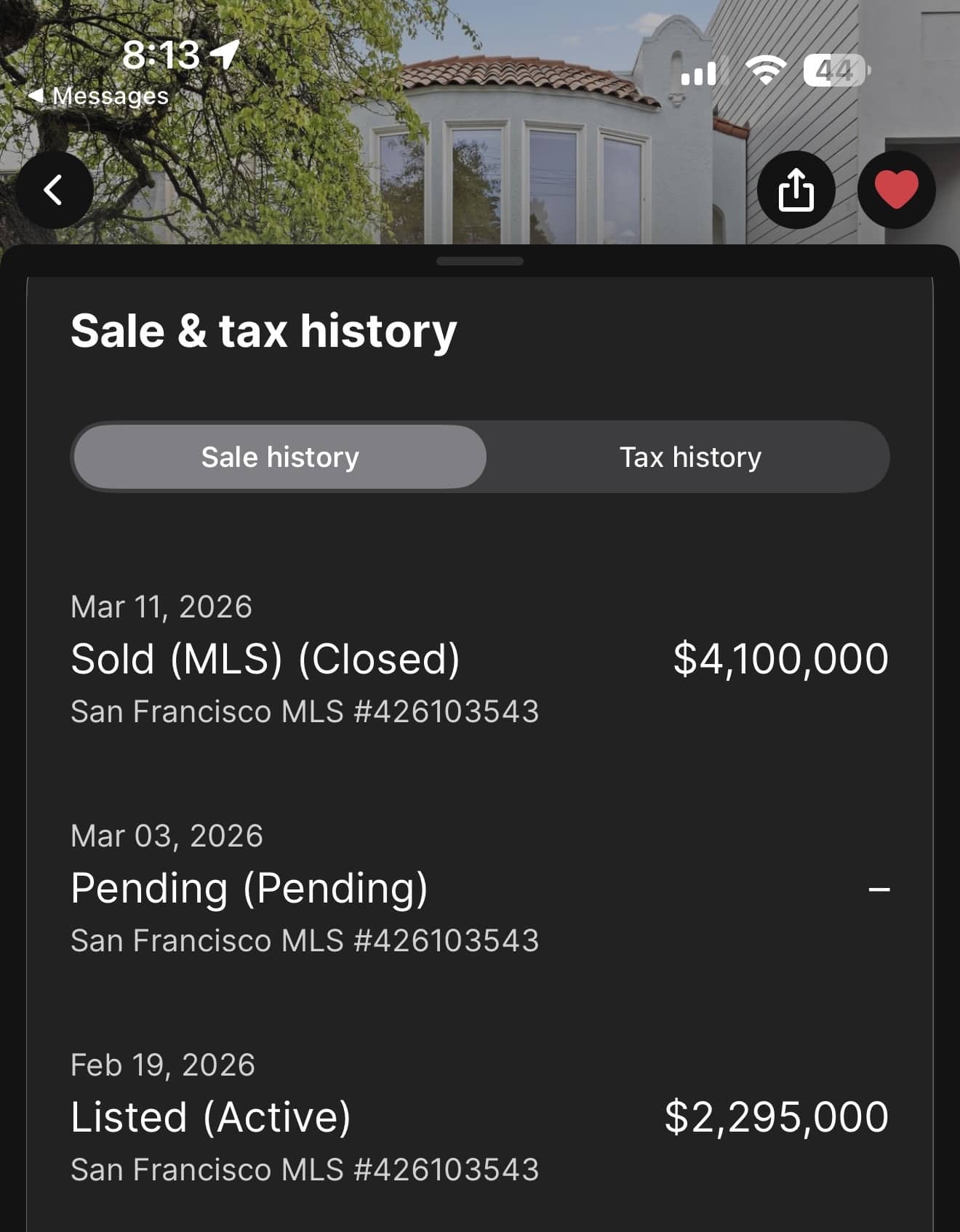

Not long ago, a residence in the picturesque Forest Hill area of San Francisco hit the market with a $2.4 million asking price. This four-bedroom, three-bathroom property spanned a humble 2,250 square feet and had undergone renovations roughly 15 years prior.

As is our custom at every open house, my wife and I placed friendly wagers on the final sale figure. She predicted $2.75 million, while I estimated $2.925 million. An overbid of $500,000, pushing the price to about $1,300 per square foot, felt plausible considering the steady stream of visitors and the appealing bay vista from the upstairs bedroom. That said, the lack of practical front or rear yard space, along with a few unusual features, tempered our optimism somewhat.

Nevertheless, about a month afterward, we learned the house fetched an astonishing $3.5 million! Initially, the news filled me with elation. Owning a similar west-side property ourselves, we instantly sensed a boost in our financial standing. Yet, as the initial euphoria from that transaction subsided, a subtle sense of letdown began to creep in.

The Sting of Selling Your House During an Upward Housing Trend

For homebuyers, the most dreaded outcome is purchasing at what turns out to be a market peak, only to witness nearby comparable properties trading at reduced values for years to come.

Fortunately, nailing the absolute top of the housing cycle demands extraordinary misfortune. Moreover, with the typical homeowner residing in their property for around 13 years on average, there's ample time to weather any downturn, even if the purchase occurs at a high point. Market slumps in real estate rarely exceed five years and frequently resolve within just two to three.

The next most regrettable housing move involves offloading your home and then observing similar—or even lesser-quality—homes in the vicinity commanding higher prices. Now, a full year after divesting my former primary home in early 2025, I'm grappling with this very sentiment amid the ongoing wave of competitive bidding frenzies.

You might encounter this emotional downturn yourself someday, making it a topic ripe for discussion. It could even prompt rationalizations, much like the ones I'm about to share, to make peace with what might feel like a less-than-ideal selling choice.

Reasons I Chose to Sell Despite Expectations of Further Price Growth

There was no pressing need to sell the home I acquired amid the 2020 lockdowns. I could have continued leasing it out, handling the inevitable upkeep and tenant-related challenges.

That notwithstanding, my positive outlook on San Francisco's real estate landscape—fueled by persistent supply shortages and the surge in artificial intelligence development—didn't stop me from listing it after just one year as a rental.

Let me outline the reasoning that led me to part with a property I wasn't compelled to sell. This introspection might assist you in navigating decisions about your own residence amid climbing property values.

1. Exhausted from Juggling Multiple Rental Holdings

Building substantial wealth through real estate often boils down to endurance—a prolonged battle of perseverance, much like certain geopolitical standoffs unfolding today. Those who outlast the competition reap the biggest rewards. Regrettably, I found myself overextended, overseeing four rentals in San Francisco alongside a vacation home in Lake Tahoe managed by a third party.

I resisted selling when the rental opportunity arose at the close of 2023, given my optimism about the Bay Area market. Instead, I gritted my teeth, spruced up the place, marketed it aggressively, and secured tenants to capture at least 12 months of potential value growth. Longer tenancy would have been a bonus.

My efforts yielded four young roommates in their mid-20s, tech professionals save for one pursuing a doctorate, complete with a cat and limited property care savvy. They weren't terrible renters, but their approach to maintenance felt casual at best. The yard grew wild, driveway walls bore scrapes, and they managed to wrench the kitchen faucet clean off, flooding the area. Rather than owning up, they claimed it spontaneously malfunctioned.

I let it slide, shelling out around $380 for a replacement fixture and another $100 for my handyman to install it.

Winter Weather Woes Add to the Burden

Following the intense downpours of the 2023-2024 winter season, I had zero desire to tackle possible leaks or felled trees for another cycle.

Years back, my neighbor below had urged me to trim a tree on the slope that threatened their yard. Acting neighborly, I brought in professionals, dropping about $600 to reduce its height and weight.

I'd already addressed leaks around west-facing window sills from exterior exposure, which were fully disclosed. Repeating those repairs, plus potentially dealing with roofing troubles, held no appeal.

Thus, when my tenants announced their departure after a year, it seemed like the universe signaling it was time to sell.

2. Overextended Financially Beyond My Comfort Level

I've been a landlord in San Francisco since 2005, enduring my share of aggravations over nearly two decades. From that experience, I pegged three as the sweet spot for self-managed city rentals.

Property managers were off the table since I lack a traditional job and leverage a network of reliable tradespeople from countless renovation endeavors. Self-maintenance keeps costs down, avoiding the steep fee of one month's rent per year.

Late 2023 saw me push boundaries by snapping up an idyllic family home on a spacious lot boasting Golden Gate Bridge views. It had lingered unsold since 2022; I coveted it then but lacked liquidity. After much deliberation, I passed. Come summer, the agent circled back with a reduced price tag. Buoyed by stock recoveries and savings buildup, I pounced, converting my prior home into a rental. Suddenly, I oversaw four urban rentals—one too many for comfort.

This meant gambling on a trouble-free year ahead.

Southern California Wildfires Prompted Action

The devastating Southern California blazes in January 2025, which obliterated entire communities in hours, crystallized my resolve against tempting disaster further. Lavish multimillion-dollar estates vanished in flames.

Reports highlighted State Farm withdrawing numerous policies beforehand, leaving some owners uninsured amid staggering losses.

Those infernos evoked memories of 2008-2009, when my net worth plunged 40% after a decade of accumulation. Peers fared worse, wiped out by leveraged stock positions and flawed diversification strategies.

As dad to a five-year-old and seven-year-old then, my plate was fuller than ever. Prioritizing family time drove my 2017 sale of another erstwhile primary home, rented out for three years beforehand.

Layer on the May 2025 debut of Millionaire Milestones, and derisking to hone my focus became paramount.

3. Relieved to Eliminate Mortgage Debt

The swiftest path to shedding mortgage obligations is selling an encumbered property, rather than piecemeal principal payments from surplus funds. Despite the modest 2.5% rate, the balance hovered near $1.4 million. The 7/1 ARM was set to reset in 2027, granting me five prime years of cheap borrowing.

$9,000 monthly rent sounded appealing, but mortgage and taxes trimmed it to roughly $3,500 net. At minimum, payments chipped away $2,500 monthly at principal.

Yet that $3,500 cash flow—or $6,000 net worth accrual—paled against ownership hazards and maintenance hassles. I'd aimed for $10,000 rent but settled lower.

Age brings a yearning for debt freedom and stability. Early mortgage payoff delivers guaranteed yields, amplified liquidity, and bolstered confidence—a true trifecta.

Rates trending lower once more.

4. Committed to Selling Only at My Ambitious Target

Bullish on local prices, I established an ambitious benchmark. My agent knew: miss it, and we hold. This mindset guarded against post-sale dissatisfaction.

In the end, a preemptive cash bid with a 10-day escrow clinched it, surpassing my goal by $18,000 post-negotiation. I accepted, though I'd fantasized about $100,000-$200,000 more. No rival emerged, despite outreach to elite agent circles over weeks.

5. Mapped Out Reinvestment Strategy for Sale Funds

Streamlining to fewer mortgages and accounts freed mental bandwidth for proceeds allocation, targeting 10% returns.

Tech optimism and 4%+ Treasuries guided choices: 70% into S&P 500 and picks like Google, Apple; the balance in T-bills and bonds at 4-5% yields.

Timing faltered—deploying in March 2025 preceded a 20% Liberation Day plunge. Heed caution on dip-chasing amid looming corrections, though I persisted, and recovery followed.

Late summer, $191,000 into Fundrise's venture fund yielded 43.5% annually. Committing $250,000 per child to 529s emboldened similar tech bets for their future.

Proceeds have topped 10% thus far, though volatility looms large.

6. Maximized Tax-Free Capital Gains Exclusion

One year rented, four of five prior as primary qualified for the full $500,000 married-filing-jointly exclusion.

A 2025 renewal tenant might extend beyond 12 months—75% odds for families—risking the two-of-five-year residency test.

Post-2008 rental periods erode proration once disqualified.

7. Retained Bay Area Real Estate Stake

Even post-sale, west-side appreciators persist via other holdings, albeit moderated gains. Honolulu move by 2029 prompts offloading two or three for lighter loads. Sole rental? No sale.

Perfect Timing Eludes Us All

Hindsight wishes tenants delayed notice to late 2025—another 5-10% uplift on a family-friendly gem for seasoned tech duos.

Priced just beyond peak frenzy, it offered value; frenzy's creep seemed inevitable.

Yet maintenance stresses—leaks, tree falls, tenant mishaps—loomed large. Spotting roofers recently hints at issues.

Now aligned at 35% stocks, 40% real estate, balance in VC, bonds, etc., peace prevails. Dropping $30,000+ annual taxes feels liberating. SF governance edges toward betterment under new leadership.

Cherishing the Home and Memories It Provided

This haven sheltered us three-plus pandemic years, expanding space amid newborn arrival and remodel delays.

Eternal thanks due. I'd have accepted breakeven post-fees—a 5% hit—grateful for its timely aid.

Reframed: not just profit vehicle, but vital lifestyle anchor with financial upside.

Shifting Toward Fully Passive Opportunities

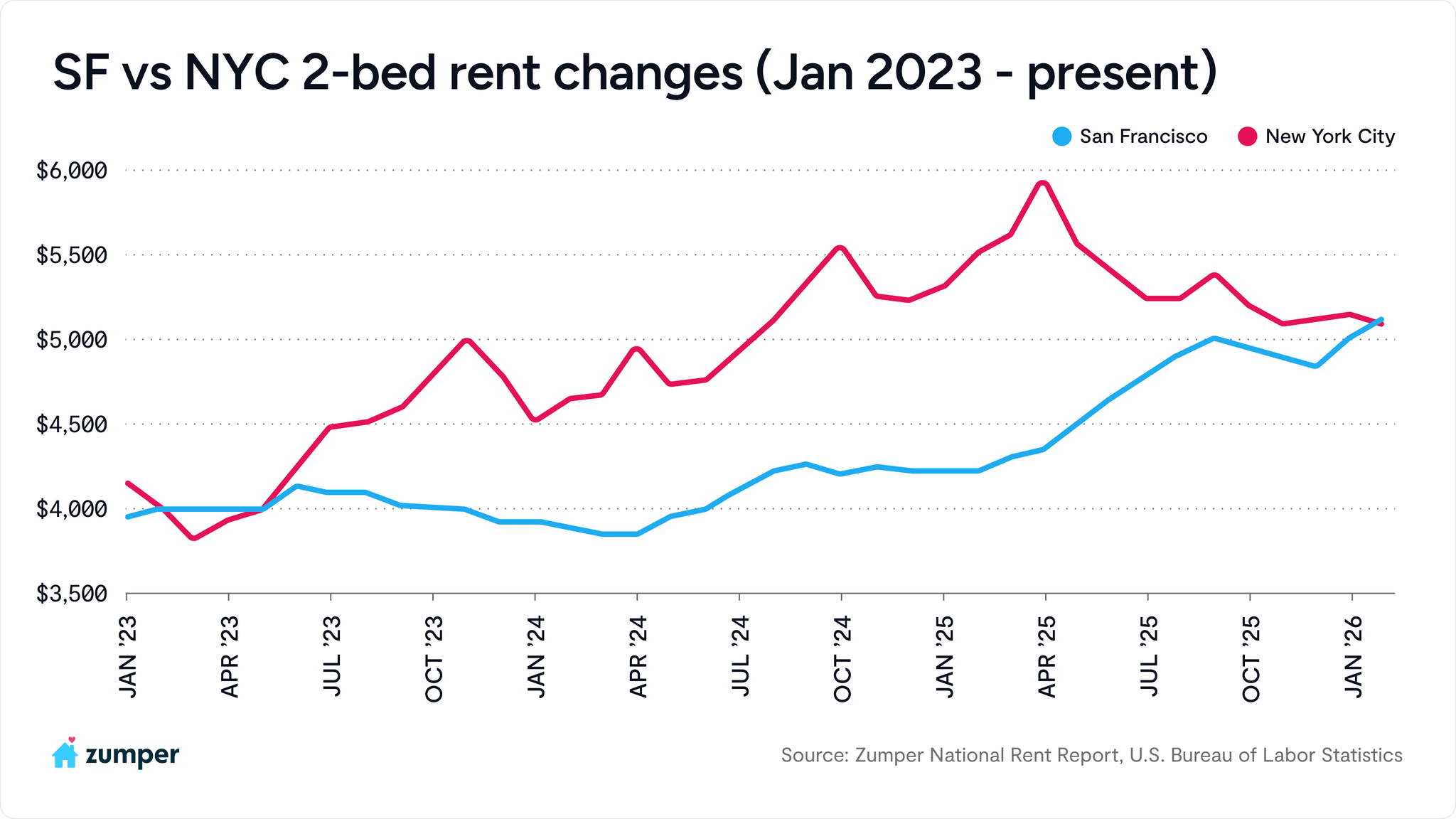

Three-plus years of stalled construction nationwide means supply absorption and rising rents ahead. SF already posts 10% yearly jumps amid startups and AI.

Maturity favors simplicity: channel proceeds to hands-off stocks, bonds, private real estate. Kids nearing independence; rental wrangling holds no allure.