Emma Taylor- I am a passionate personal finance blogger dedicated to helping individuals take control of their financial well-being.

Emma Taylor- I am a passionate personal finance blogger dedicated to helping individuals take control of their financial well-being.How to Create a Budget for Purchasing a HomePurchasing your first home is an incredibly thrilling milestone, filled with endless possibilities and choices. Do you envision living in a bustling urban area or a peaceful rural setting? Would you prefer a spacious ranch-style property or a cozy townhous

How to Create a Budget for Purchasing a Home

Purchasing your first home is an incredibly thrilling milestone, filled with endless possibilities and choices. Do you envision living in a bustling urban area or a peaceful rural setting? Would you prefer a spacious ranch-style property or a cozy townhouse? Are you drawn to a charming fixer-upper project or a pristine move-in-ready residence?

Regardless of your preferences, the cornerstone of successful homeownership lies in selecting a property that aligns perfectly with your financial capabilities. Developing a solid home budget serves as the essential foundation for achieving this goal without compromising your financial stability.

The great news is that crafting an effective house budget doesn't demand advanced credentials in economics or sophisticated financial knowledge. It's accessible to everyone and boils down to adhering to a straightforward five-step process that anyone can master with ease.

Let's explore these steps in detail to empower you on your journey toward homeownership.

Before we delve into the specifics of building your home budget, it's crucial to emphasize a vital prerequisite: you should only pursue buying a house once you have eliminated all consumer debt and established a robust emergency fund. Without these safeguards, the responsibilities and unexpected costs of homeownership—such as appliance failures or structural repairs—could spiral into overwhelming financial distress.

Imagine a scenario where a malfunctioning refrigerator or a damaged roof transforms a minor inconvenience into a major budgetary catastrophe. To prevent this, prioritize clearing all debts and building an emergency reserve covering three to six months of your standard living expenses before proceeding with your home budgeting plan.

With those foundational elements in place, you'll be well-equipped to follow the five steps outlined below, creating a reliable roadmap for affording your new home comfortably.

Step 1: Establish Your Savings Target

The initial phase in budgeting for a house involves determining your savings objective by reflecting on three fundamental questions that guide your financial planning.

- What is the maximum house price you can realistically afford? A practical rule of thumb is to take your monthly net income—after taxes and deductions—and divide it by four. This figure represents the comfortable upper limit for your total monthly housing payment, encompassing principal, interest, homeowners insurance, and any applicable homeowners association fees, assuming a 15-year fixed-rate mortgage. Exceeding 25% of your take-home pay risks leaving you house poor, strained by housing costs. Tools like a mortgage calculator can provide precise estimates of monthly payments across various home prices and interest rates.

- What down payment amount are you aiming for? For those entering the market as first-time buyers, target saving at least 5–10% of the home's purchase price. However, stretching to a 20% down payment offers significant advantages, such as avoiding private mortgage insurance, which adds unnecessary expense. A larger initial investment also translates to reduced monthly mortgage obligations, easing your long-term financial load. Additionally, allocate funds for closing costs and potential incidental expenses that arise during the transaction.

- What is your desired timeline for home purchase? Your budgeting strategy will vary based on your timeframe. If you're aggressively aiming to buy within 10 months, you'll need an intensified savings pace. Conversely, if your purchase is several years away, you can adopt a more gradual approach without the pressure of extreme measures.

Once you've answered these, perform the necessary calculations to determine your required monthly savings. Simply divide your targeted down payment total by the number of months in your savings period.

Consider this illustrative example: A married couple with a combined annual income of $130,000 decides to pursue an ambitious 33% down payment on a $300,000 home over two years, factoring in a 5.5% interest rate to ensure manageable monthly payments.

Their detailed savings goal breakdown would appear as follows:

You might initially view $200,000 as insufficient for a substantial home, but market realities often necessitate adjustments, particularly for first-time buyers. Home prices have surged dramatically in recent years, making it unlikely to secure your ideal property immediately.

Embrace the idea of starting with a modest, budget-friendly home, even if it means compromising on size or neighborhood. This prudent choice will spare you future regret from overextending financially for aesthetic appeal. Remember, you can always trade up later when your circumstances allow for greater spending power.

Skeptical about the feasibility of saving $100,000? As we progress through this example, the numbers will demonstrate just how attainable such goals can be with disciplined planning.

Step 2: Document Your Monthly Income

With your savings target defined, proceed to the next phase by meticulously recording your after-tax income from all sources. Understanding your total available funds is indispensable for constructing a viable budget.

Take time to tally every income stream, including primary wages, supplemental side gigs, and any other predictable earnings for the month. This comprehensive approach ensures every dollar is accounted for in your planning.

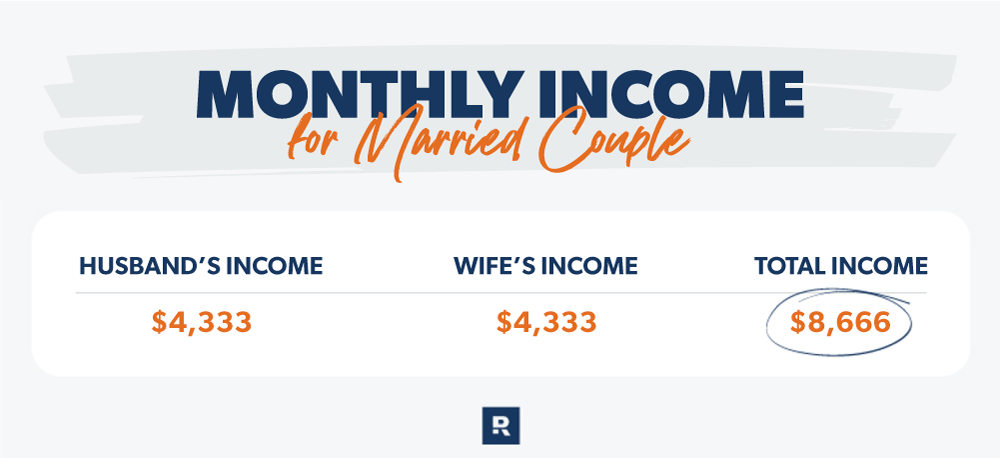

For our example couple, this income summary takes shape like this:

Straightforward and illuminating, wouldn't you agree? This clarity forms the bedrock of effective budgeting.

Step 3: Outline Your Expenses

Now that your income is quantified, shift focus to mapping out where every dollar will be allocated by cataloging your recurring monthly expenditures. If you're accustomed to monthly budgeting, this step is familiar territory. For newcomers, rest assured it's simpler than it appears.

Begin with essentials: groceries, commuting costs, shelter, and utilities—the unavoidable necessities. Then, expand to other significant areas like recurring subscriptions, apparel, leisure activities, vehicle upkeep, dining out, and charitable giving. Crucially, designate a specific category for your house savings goal derived from Step 1.

To assign realistic amounts, review your recent bank statements and purchase records for insights into actual spending patterns. Integrate your house savings figure precisely into the budget.

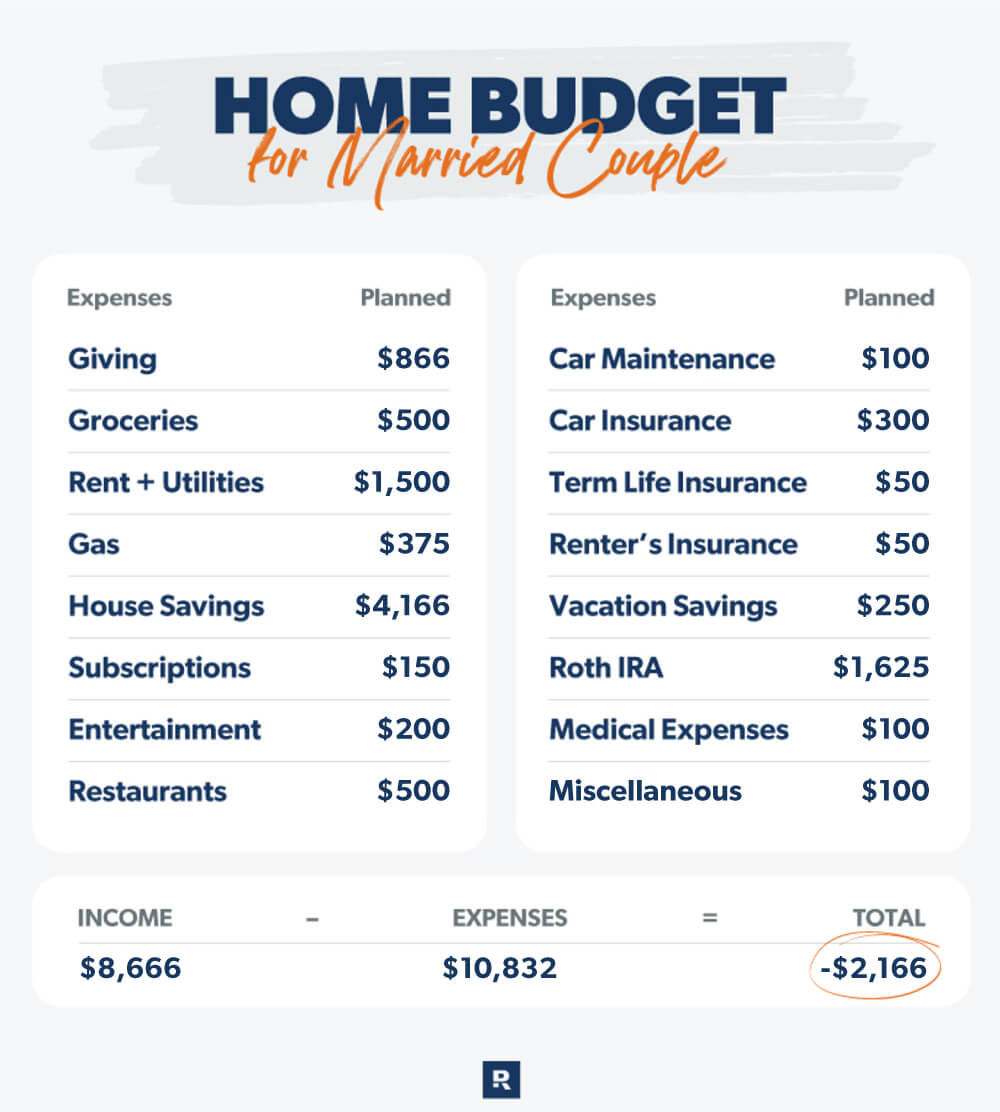

Returning to our $65,000-per-spouse couple, their preliminary home budget after this exercise might resemble the following:

Notice the imbalance? Their planned outflows exceed inflows, a common initial outcome. The subsequent step addresses this effectively.

Step 4: Implement Necessary Adjustments

First-time budgets frequently reveal expenditures surpassing income, mirroring our couple's situation. Resolve this by either boosting revenue or trimming costs—or ideally, both.

Enhance income through avenues like part-time side hustles, overtime opportunities, or decluttering and selling unused possessions.

For expense reduction, consider these proven strategies tailored for home savers:

- Pause retirement contributions temporarily. While consistent retirement saving is vital long-term, it's permissible to redirect funds toward your house goal for up to three years. Resume investing 15% of income immediately post-purchase to stay on course.

- Prioritize home-cooked meals. Dining out occasionally is fine, but minimizing restaurant visits frees substantial funds—compensate by slightly increasing your grocery allowance.

- Curate your subscriptions wisely. The proliferation of streaming platforms can erode budgets swiftly. Eliminate redundancies; ample free alternatives exist, rendering multiple paid services unnecessary.

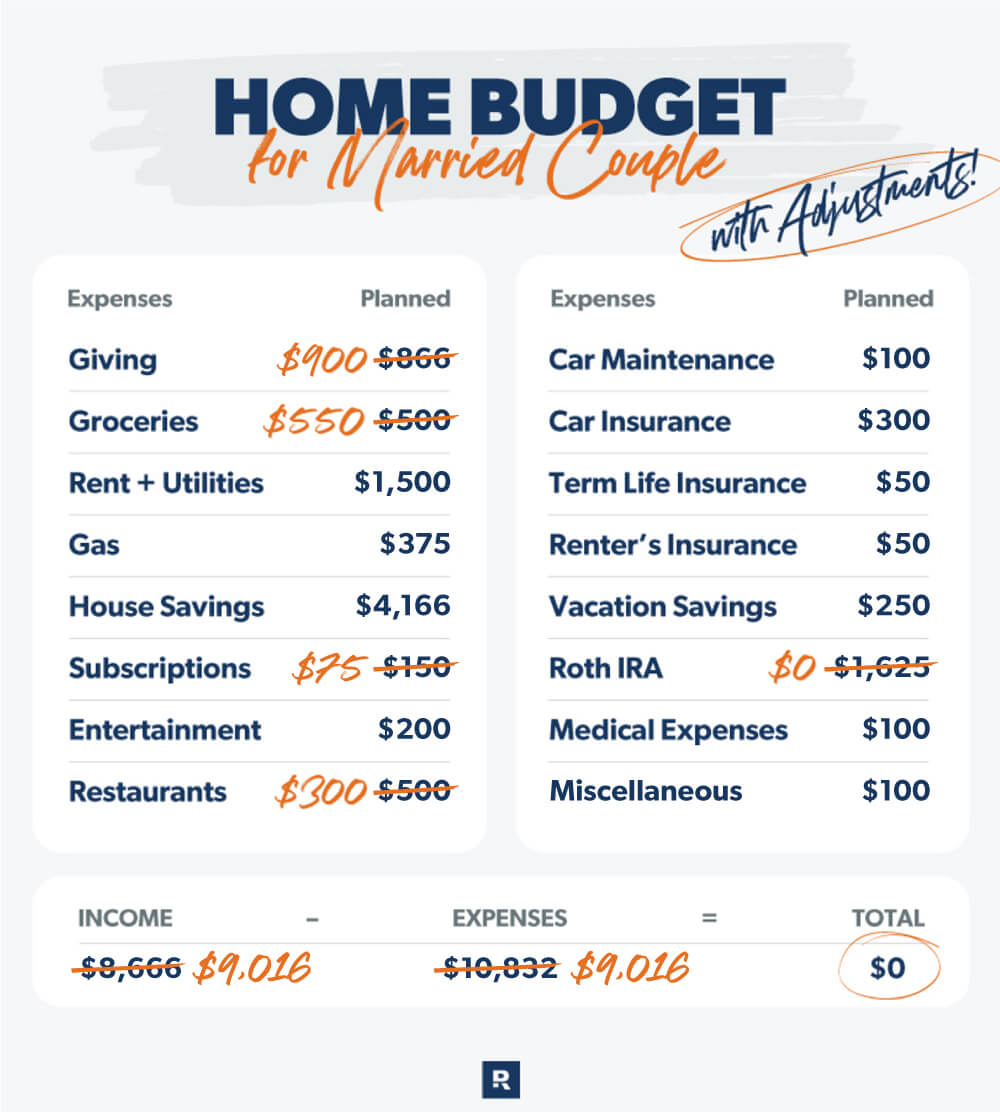

These modest shifts yield impressive results. In our example, the couple applies all three cuts, plus each launches a side hustle netting $175 extra monthly. Their revised budget transforms dramatically:

Remarkable progress! Minor modifications shifted them from a $2,000+ deficit to a balanced, zero-based budget, positioning them for that substantial 33% down payment in two years.

Step 5: Monitor and Maintain Progress

Creating the budget is merely the beginning; sustained success demands diligent adherence and regular tracking. Review transactions monthly to ensure alignment with allocated categories.

Budgeting apps streamline this by automating transaction imports from linked accounts, eliminating manual entry hassles and providing real-time oversight.

You're Well on Your Way!

Consistent budgeting will propel you toward your savings milestone, hastening readiness for homeownership. To recap the essentials:

- Calculate your affordable home price using reliable tools.

- Define your precise savings goal.

- Build and maintain your budget with user-friendly applications.

Frequently Asked Questions

Where is the best place to store my down payment savings?

Opt for a money market account or high-yield savings account. These provide stability without risk of loss, maintaining liquidity for easy access when needed.

When is the ideal time to begin saving for a house?

Commence immediately after achieving debt freedom and securing a 3–6 month emergency fund covering your usual expenses.

How much should you save prior to buying a house?

Aim for a minimum 5–10% down payment, plus reserves for closing costs and unforeseen fees. A 20% down payment is optimal, sidestepping private mortgage insurance entirely.